Left Semi Join Engine

DolphinDB provides multiple lightweight and easy-to-use join engines. This page will introduce window join engine.

Introduction

Similar to the SQL equi join, the left semi join engine pairs

records from the left and right tables based on matching column values. For each

record from the left table, the engine caches it until a record with the same

matching column value is found in the right table. The join is triggered only when a

match is identified.

Unlike the SQL equi join, the engine only caches the first or last

record with the same matching column value in the right table. As a result, each

left record is joined at most once.

The following figure depicts how the left semi join engine (which retains the latest record for each join column value from the right table) processes ingested streams. Each stream contains two columns: a join column and a metrics column.

For application scenarios of the engine, see Section "Left Semi Join Engine: Joining Trades With Orders Data" and "Left Semi Join Engine: Correlating Individual Stocks to Index".

createLeftSemiJoinEngine(name, leftTable, rightTable, outputTable, metrics, matchingColumn, [garbageSize=5000], [updateRightTable=false])Details about the parameters, see: createLeftSemiJoinEngine.

Use Case 1: Joining Trades With Orders Data

In this use case, we will enrich trading information by joining tick trades with buy and sell orders based on the order IDs. The trade record is only output after its corresponding orders are found.

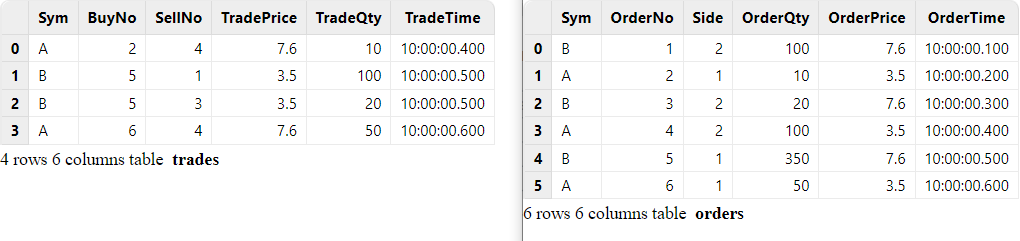

We create a streaming cascade with two left semi join engines to associate trades with buy and sell orders. We create four stream tables for trades, orders, output intermediate results, and the final output.

// create table

share streamTable(1:0, `Sym`BuyNo`SellNo`TradePrice`TradeQty`TradeTime, [SYMBOL, LONG, LONG, DOUBLE, LONG, TIME]) as trades

share streamTable(1:0, `Sym`OrderNo`Side`OrderQty`OrderPrice`OrderTime, [SYMBOL, LONG, INT, LONG, DOUBLE, TIME]) as orders

share streamTable(1:0, `Sym`SellNo`BuyNo`TradePrice`TradeQty`TradeTime`BuyOrderQty`BuyOrderPrice`BuyOrderTime, [SYMBOL, LONG, LONG, DOUBLE, LONG, TIME, LONG, DOUBLE, TIME]) as outputTemp

share streamTable(1:0, `Sym`BuyNo`SellNo`TradePrice`TradeQty`TradeTime`BuyOrderQty`BuyOrderPrice`BuyOrderTime`SellOrderQty`SellOrderPrice`SellOrderTime, [SYMBOL, LONG, LONG, DOUBLE, LONG, TIME, LONG, DOUBLE, TIME, LONG, DOUBLE, TIME]) as output

// create engine: left join buy order

ljEngineBuy=createLeftSemiJoinEngine(name="leftJoinBuy", leftTable=outputTemp, rightTable=orders, outputTable=output, metrics=<[SellNo, TradePrice, TradeQty, TradeTime, BuyOrderQty, BuyOrderPrice, BuyOrderTime, OrderQty, OrderPrice, OrderTime]>, matchingColumn=[`Sym`BuyNo, `Sym`OrderNo])

// create engine: left join sell order

ljEngineSell=createLeftSemiJoinEngine(name="leftJoinSell", leftTable=trades, rightTable=orders, outputTable=getLeftStream(ljEngineBuy), metrics=<[BuyNo, TradePrice, TradeQty, TradeTime, OrderQty, OrderPrice, OrderTime]>, matchingColumn=[`Sym`SellNo, `Sym`OrderNo])

// subscribe topic

subscribeTable(tableName="trades", actionName="appendLeftStream", handler=getLeftStream(ljEngineSell), msgAsTable=true, offset=-1)

subscribeTable(tableName="orders", actionName="appendRightStreamForSell", handler=getRightStream(ljEngineSell), msgAsTable=true, offset=-1)

subscribeTable(tableName="orders", actionName="appendRightStreamForBuy", handler=getRightStream(ljEngineBuy), msgAsTable=true, offset=-1) In this script, the engine "leftJoinSell" joins "trades" and "orders" based on the sell order IDs. The output of "leftJoinSell" is then ingested as the left stream into the engine "leftJoinBuy" to be joined with the right stream of "orders" based on buy order IDs.

To manage the memory usage of engines, we use the default value of the parameter garbageSize. Unlike other engines, the left semi join engine only clears the unneeded historical data from the left table and maintains all records from the right table in the cache. Thus, each engine created above is at least the size of the "orders" table.

The following script appends "orders" to the right stream and "trades" to the left stream of the engine "leftJoinSell":

// generate data: trade

t1 = table(`A`B`B`A as Sym, [2, 5, 5, 6] as BuyNo, [4, 1, 3, 4] as SellNo, [7.6, 3.5, 3.5, 7.6]as TradePrice, [10, 100, 20, 50]as TradeQty, 10:00:00.000+(400 500 500 600) as TradeTime)

// generate data: order

t2 = table(`B`A`B`A`B`A as Sym, 1..6 as OrderNo, [2, 1, 2, 2, 1, 1] as Side, [100, 10, 20, 100, 350, 50] as OrderQty, [7.6, 3.5, 7.6, 3.5, 7.6, 3.5] as OrderPrice, 10:00:00.000+(1..6)*100 as OrderTime)

// input data

orders.append!(t2)

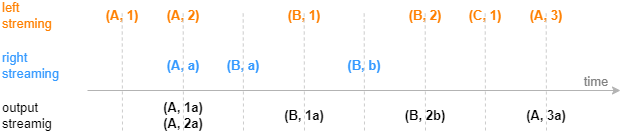

trades.append!(t1)The correspondence of records between the input streams is shown below:

The output table shows that each trade record is joined with its corresponding buy and sell order records from the "orders" stream. It now displays information on the buy and sell quantity, price, and time for each trade.

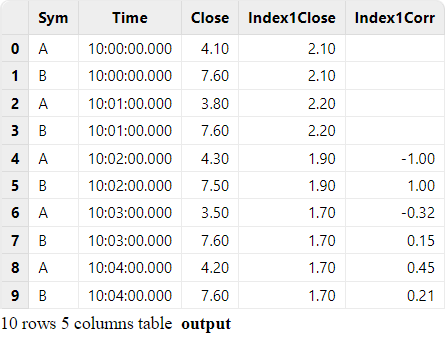

Use Case 2: Correlating Individual Stocks to Index

This use case correlates individual stocks to a stock index. The stock and index data are downsampled to 1-minute interval. All stocks are associated with one index, and a join result is output for each input stock record.

To achieve this, we cascade a left semi join engine with a reactive state engine.

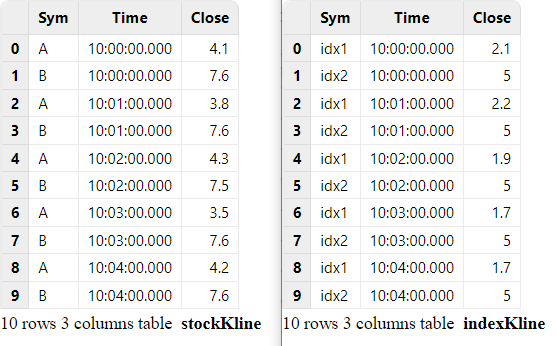

// create table

share streamTable(1:0, `Sym`Time`Close, [SYMBOL, TIME, DOUBLE]) as stockKline

share streamTable(1:0, `Sym`Time`Close, [SYMBOL, TIME, DOUBLE]) as indexKline

share streamTable(1:0, `Time`Sym`Close`Index1Close, [TIME, SYMBOL, DOUBLE, DOUBLE]) as stockKlineAddIndex1

share streamTable(1:0, `Sym`Time`Close`Index1Close`Index1Corr, [SYMBOL, TIME, DOUBLE, DOUBLE, DOUBLE]) as output

// create engine: calculate correlation

rsEngine = createReactiveStateEngine(name="calCorr", dummyTable=stockKlineAddIndex1, outputTable=output, metrics=[<Time>, <Close>, <Index1Close>, <mcorr(ratios(Close)-1, ratios(Index1Close)-1, 3)>], keyColumn="Sym")

// create engine: left join Index1

ljEngine1 = createLeftSemiJoinEngine(name="leftJoinIndex1", leftTable=stockKline, rightTable=indexKline, outputTable=getStreamEngine("calCorr"), metrics=<[Sym, Close, indexKline.Close]>, matchingColumn=`Time)

// subscribe topic

def appendIndex(engineName, indexName, msg){

tmp = select * from msg where Sym = indexName

getRightStream(getStreamEngine(engineName)).append!(tmp)

}

subscribeTable(tableName="indexKline", actionName="appendIndex1", handler=appendIndex{"leftJoinIndex1", "idx1"}, msgAsTable=true, offset=-1, hash=1)

subscribeTable(tableName="stockKline", actionName="appendStock", handler=getLeftStream(ljEngine1), msgAsTable=true, offset=-1, hash=0)In this case, the user-defined function appendIndex is specified as the

handler of the subscription to "indexKline", which selects index "idx1"

and publishes the filtered stream to the join engine. The "leftJoinIndex1" engine

joins stock data "stockKline" with filtered index data. The output of

"leftJoinIndex1" is then ingested into the reactive state engine "calCorr" which

uses the built-in state functions mcorr and ratios

to calculate stock correlation.

The following script appends "indexKline" to the right stream and "stockKline" to the left stream:

// generate data: stock Kline

t1 = table(`A`B`A`B`A`B`A`B`A`B as Sym, 10:00:00.000+(0 0 1 1 2 2 3 3 4 4)*60000 as Time, (4.1 7.6 3.8 7.6 4.3 7.5 3.5 7.6 4.2 7.6) as Close)

// generate data: index Kline

t2 = table(`idx1`idx2`idx1`idx2`idx1`idx2`idx1`idx2`idx1`idx2 as Sym, 10:00:00.000+(0 0 1 1 2 2 3 3 4 4)*60000 as Time, (2.1 5 2.2 5 1.9 5 1.7 5 1.7 5) as Close)

// input data

indexKline.append!(t2)

stockKline.append!(t1)The correspondence of records between the input streams is shown below:

As shown in the output table, both the stocks A and B are correlated to index idx1.

The result of the first two minutes is empty because the window size of

mcorr is 3.